This project is implemented in partnership with Dialogue Bureau Foundation and Green Think Tank

Infographics by Ksenia Storozheva

Executive Summary

- Since 2022, the EU has banned seaborne imports of Russian oil; consequently, Russia's share of supplies decreased to approximately 1% in Q3 2025, down from 29% in Q1 2021. Regarding EU natural gas imports, Russia’s share fell to ~15% in Q3 2025 from ~40% in Q1 2021.

- In response, Russia reoriented its exports toward Asia: China and India now account for up to ~80% of all Russian oil shipments. India has emerged as the largest spot-market buyer, while China serves as a strategic partner under long-term contracts.

- Sanctions did not lead to a sharp decline in production, but export costs rose significantly due to discounts, extended logistics, and expenditures on circumventing restrictions, including the formation of a "shadow fleet." The Urals-to-Brent discount increased to ~$15–20 per barrel or higher, compared to ~$3 per barrel prior to 2022.

- Export revenue declined moderately: in 2023–2024, it fell by only 3.3% compared to 2018–2019 levels. Revenues remain largely determined by global prices and the ruble exchange rate, as sanction-induced shocks proved to be short-term.

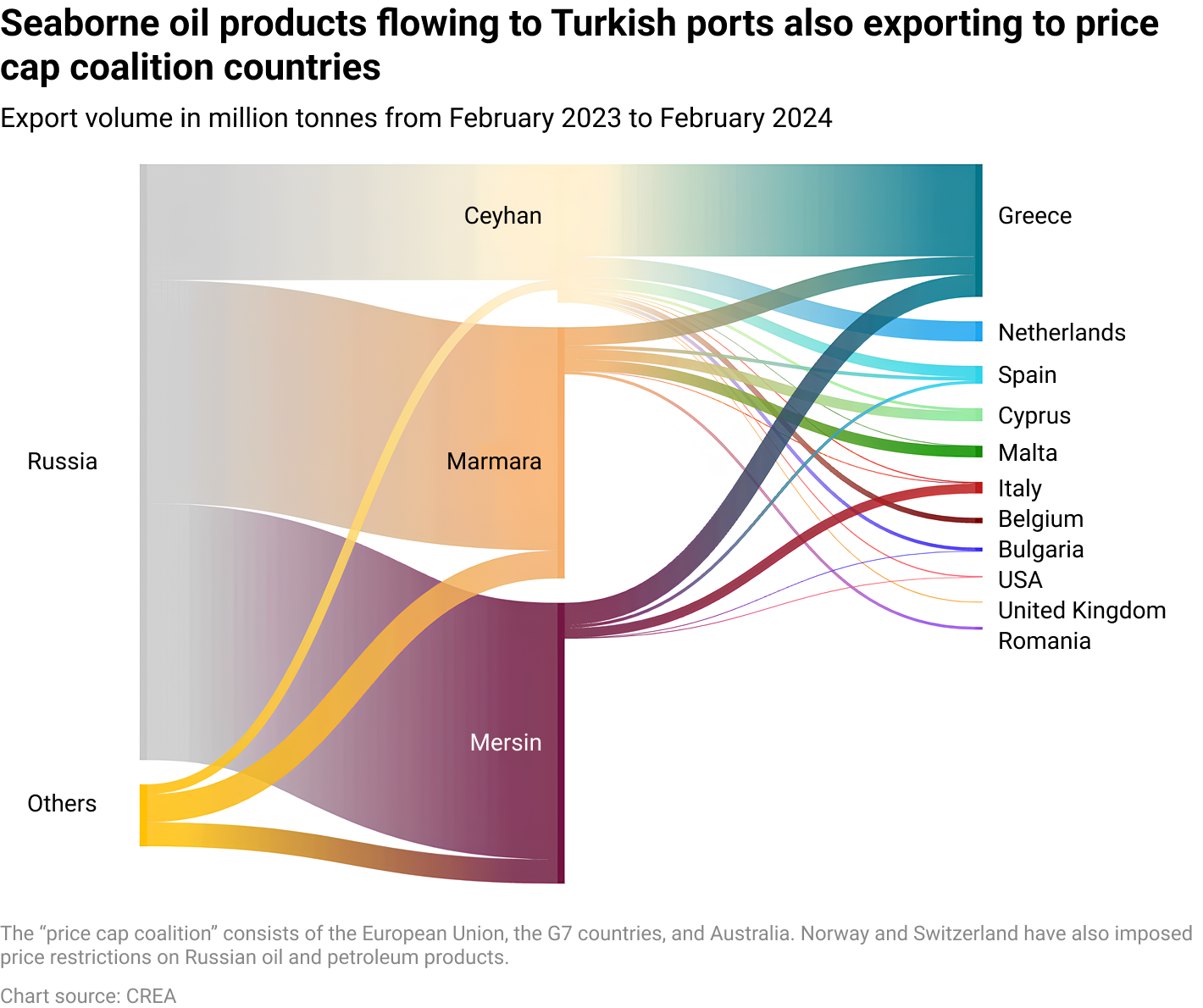

- Concurrently, a "refining loophole" persists: a portion of Russian feedstock returns to the European market via processing and re-export from third countries as petroleum products with formally altered countries of origin. Thus, the EU maintains a link—albeit a limited one—to Russian oil.

- Turkey and India have become the refining loophole primary hubs. EU petroleum product imports from Turkey increased by 107% year-on-year between February 2023 and February 2024, reaching approximately 13 million tonnes, which accounted for roughly 11% of total EU petroleum product imports during that period. EU petroleum product imports from India rose from $8.7 billion in 2021–22 to $19.2 billion in 2023–24, making India the EU's largest supplier of petroleum products in 2024. While the exact proportion of Russian crude oil used for these shipments cannot be determined, estimates suggest that approximately one-third of the petroleum products exported to the EU from India, and the majority of shipments from Turkey, were produced from Russian feedstock. To resolve this problem, the 18th sanctions package was adopted, tightening EU customs controls.

- The Russian government's "fiscal maneuver" shifted the tax burden from export volumes to oil production volumes. Budgetary dependence on oil revenues has been reduced (to ~20% in 2025–2027, down from 39% in 2019 and 36% in 2021), as the fiscal load is gradually redistributed to other economic sectors.

- Following the US imposing sanctions against Russian oil companies, India began refusing feedstock purchases in December 2025; it is expected that intake may decrease by approximately half, to 0.8–1 million barrels per day or lower.

- Trends of 2025 indicate that sanction pressure will shift toward individual sanctions against shadow fleet vessels and secondary sanctions against Russia's trading partners. Simultaneously, instead of an oil price cap, G7+ countries and the European Commission are discussing a total ban on maritime services for Russian oil exports. In addition to further complicating Russian trade, such measures will facilitate the consolidation of an alternative market outside the control of the G7+ coalition.

- The US-Israeli war against Iran and the blockade of the Strait of Hormuz resulted in a doubling of Russian crude oil prices between March and May 2026. This drove oil and gas budget revenues up twofold in April and by 1.5 times in March and May relative to the average monthly figures for January and February.

- Nevertheless, owing to ruble appreciation, oil and gas revenues for January–May 2026 came in at nearly one-third below the figures recorded for the same period in 2025. For the same reason, elevated oil prices will not resolve the fiscal challenges facing the federal budget, whose deficit is projected by the Ministry of Finance to increase by one and a half times over the course of the year relative to the figure stipulated in the budget law.

- Sanctions targeting petroleum products manufactured in third countries from Russian crude oil have reduced Russian oil companies' export revenues from this category by half.

Introductory Note

While this report was being prepared for publication, developments on the global stage altered the scenario conditions for the world oil market. The US-Israeli military operation against Iran partially offset, in the short term, the impact of sanctions on Russia's oil sector — hydrocarbon prices doubled and a number of export restrictions were lifted. This does not resolve the fiscal challenges facing the Russian federal budget: owing to high military expenditures — which account for 30% of budgetary appropriations — the budget deficit for 2026 will not narrow but is projected to widen by one and a half times, reaching 2.5% of GDP.

From March 2026, immediately following the outbreak of hostilities, the Strait of Hormuz was blockaded — a waterway through which approximately 20% of global oil production is transported — and airstrikes against energy infrastructure across the Persian Gulf region commenced. As a result, Brent crude prices rose by 38% by early June compared to the second half of February, climbing from $68 to $94 per barrel. On individual days in March, April, and May, the benchmark price exceeded $100–110 per barrel.

Accordingly, the FOB price of all grades of Russian crude at all ports doubled relative to pre-war levels in January and February 2026. Urals discounts to Brent remained elevated for shipments from western ports and minimal for those from eastern ports. Specifically, the Urals-to-Brent FOB discount for Baltic and Black Sea loadings averaged $22–25 per barrel in March–May, while select cargoes bound for India and China were sold at a premium of $1.5–6 per barrel. The discount on ESPO-grade cargoes from Pacific ports stood at $2–6 per barrel.

Accounting for these discounts, the average FOB Primorsk price in March–May rose to $90 per barrel from $43 in mid-February, while FOB ESPO climbed to $93 from $55 prior to the war.

A further positive factor supporting Russian crude prices at elevated levels was the partial easing of sanctions. In particular, beginning in March, the United States issued licenses permitting energy buyers to purchase Russian crude, renewing these licenses on a monthly basis. The most recent license was issued on 18 May 2026.

According to Ministry of Finance data, these combined factors drove federal budget oil and gas revenues above pre-war monthly levels. Total oil and gas revenues increased by 50% in March 2026 to RUB 617 billion, twofold in April to RUB 856 billion, and by 64% in May to RUB 679 billion, relative to the January–February 2026 monthly average of RUB 413 billion.

However, two additional factors offset, on an annual basis, the effect of abnormally high energy prices and constrained the revenues of both oil companies and the Russian federal budget.

The first was ruble appreciation: following a brief spike to RUB 87 per dollar in March, the exchange rate strengthened by 8% against the dollar by end-May compared to end-February, reaching RUB 70–72. The second was Ukrainian drone strikes against Russian ports and oil refineries.

From late March onward, Ukrainian Armed Forces (UAF) conducted multiple strikes per week against Russia's largest refineries. As a result, refining capacity equivalent to approximately 23% of Russia's total throughput was taken offline in the first half of May, rising to 29% by end-May — a conservative estimate by one of the report's co-authors that accounts only for confirmed refinery shutdowns and excludes facilities that sustained strikes for which damage data were unavailable. In addition, during spring 2026 the UAF carried out more than ten successful strikes against major oil export terminals, including Primorsk, Ust-Luga, Novorossiysk, and Tuapse, causing recurring disruptions to loading operations.

The strikes created significant sales difficulties for oil companies. Against the backdrop of a 9% year-on-year decline in petroleum product output in April 2026 (per Rosstat), Russian oil production fell by 5% year-on-year in the same month to 8.8 million barrels per day, according to the International Energy Agency (IEA).

As a result, federal budget oil and gas revenues for January–May 2026 contracted to RUB 2.98 trillion, a decline of 30% year-on-year.

A further reason why elevated oil prices in March–May failed to outweigh budget-adverse factors was the scale of subsidy payments to oil-producing companies in the form of refining support, designed to prevent domestic fuel prices from rising above the rate of inflation. Over the first five months of the year, such payments — comprising the fuel damper mechanism, the reverse excise duty, and the investment premium — totalled RUB 955 billion. The peak of RUB 757 billion fell in April and May 2026, precisely because of high prices: the costlier hydrocarbons are on global markets, the larger the compensation the Ministry of Finance pays to oil producers from the federal budget.

A further blow to the Russian budget was dealt by sanctions, introduced from 21 January 2026 onward, targeting petroleum products manufactured from Russian crude in third countries — the so-called refining loophole. These sanctions concern shipments from Turkish and Indian refineries that purchase and process Russian feedstock. According to the authors' calculations based on data from the monitoring organisation CREA, such exports to the sanctioning countries (the EU, the United States, the United Kingdom, Australia, and New Zealand) fell by half in Q1 2026 compared to Q4 2025, to $483 million. Over the full January–May 2026 period, such re-exports totalled $929 million.

The EU introduced new restrictions against a number of Russian oil companies and tankers under its 20th sanctions package in April, is planning additional measures for June, and is also considering a ban on seaborne crude shipments from Russia.

Negative factors likewise predominated for oil company profitability. Rosneft's net profit in Q1 2026 declined by 32% year-on-year to RUB 115 billion, while Gazprom Neft's fell by 3% (other companies have not published their financial statements).

Despite analyst consensus projections placing the average oil price in 2026 at a high of $90 per barrel — implying a Urals price of approximately $70 per barrel — the Russian budget is unlikely to benefit, as the constellation of negative factors is expected to continue dominating. The principal reason Russia has not captured windfall revenues from this conflict is ruble strength. Sustained demand for the national currency is underpinned by several factors: the central bank's elevated policy rate, a trade surplus that, while declining, remains substantial, a high share of foreign trade settlements denominated in rubles (estimated by the CBR at around 60%), and capital controls.

According to economist Dmitry Polevoy, the average annual ruble-to-dollar exchange rate is projected at approximately RUB 75–76, in which case the federal budget deficit could approach 2.5% of GDP — substantially above the 1.6% of GDP stipulated in the budget law for 2026. The Ministry of Finance has already acknowledged this, and is preparing to revise its fiscal parameters upward. Under this scenario, the Ministry of Finance would need to raise an additional RUB 1–1.5 trillion to finance budgetary expenditures, according to Polevoy's estimates.

On the basis of the prevailing factors, therefore, it can be concluded that elevated oil prices will not resolve the expenditure pressures facing the federal budget, nor will they augment financing for the military-industrial complex.

Despite Vladimir Putin's demands that the government achieve economic growth, expert expectations are pessimistic. In mid-May, the government published its updated macroeconomic forecast for 2026, projecting GDP growth of just 0.4%. This figure is barely distinguishable from statistical noise, particularly given that the economy expanded by an equally modest 1% in 2025.

It bears emphasis that even this marginal growth is entirely attributable to the military-industrial complex — an assessment shared even by economists close to the government. According to Rosstat, industrial output in Russia grew by 1.9% in April 2026 year-on-year; however, calculations by the pro-government Centre for Macroeconomic Analysis and Short-Term Forecasting indicate that civilian sectors contracted by 2.9% over the same period.

Against this backdrop, it is unsurprising that the government is discussing cuts to "non-sensitive" federal budget line items — a measure necessary to maintain MIC funding at its current level. All of this supports the conclusion that 2026 may prove a turning point for the Russian economy, at which recession becomes unavoidable.

The Sanctions Regime Against Russian Oil Post-2022

Russia's full-scale invasion of Ukraine in 2022 and subsequent Western sanctions have abruptly altered the export destinations for Russian hydrocarbons. The Russian economy has entered into political and economic confrontation with the EU, the US, and other leading Western economies.

In the spring of 2022, the European Commission (EC) estimated the share of Russian gas in total EU imports at approximately 50%. Furthermore, Russia accounted for approximately 25% of oil imports and 45% of coal imports to the EU. The EU, heavily dependent on Russian energy carriers, sought to eliminate this dependency and develop a strategy for the gradual phase-out of Russian gas, oil, and coal.

This was the primary objective of the REPowerEU plan, first introduced by the EC in May 2022. It included identification of new liquefied natural gas (LNG) importers, acceleration of the development and implementation of alternative gases and renewable energy sources, enhancement of end-user energy efficiency, and support for EU member states with the lowest levels of energy dependency.

In parallel with the development of this plan, the EU initiated sanction pressure on Russia aimed at reducing its hydrocarbon export revenues. As early as February 2022, the Council of the European Union adopted the initial packages of energy sanctions against Russia; by the end of the year, nine packages had been implemented. As of October 2025, the number of packages has reached nineteen.

The EU introduced a total ban on coal imports and established an embargo on seaborne tanker imports of crude oil. Hungary, Slovakia, Bulgaria, and the Czech Republic (the latter two only until 2025) were permitted, by way of exception, to receive Russian crude oil via the Druzhba pipeline. The EU did not prohibit pipeline gas supplies from Russia (these decreased unilaterally following a decision by Gazprom intended to exert pressure on European buyers) and even increased imports of Russian LNG. However, the EU has begun a gradual phase-out of LNG, although a total ban on entering into new long-term LNG supply contracts will only take effect on January 1, 2027. Additionally, the EU introduced measures against the transit of Russian LNG through European terminals.

In one way or another, the EU is actively diversifying its oil and gas suppliers. Based on the results of the first half of 2025, the largest suppliers of pipeline gas were Norway (55% of imports), Algeria (19%), and Russia (10%), while for LNG, the leaders were the USA (57%), Russia (13%), Qatar (8%), and Algeria (7%). In the first three quarters of 2025, the EU's primary partners for oil imports were Norway (14%), the USA (14%), and Kazakhstan (12%).

In January 2026, EU countries approved a plan for a complete phase-out of Russian gas within two years. Under short-term contracts, the purchase of LNG is prohibited starting April 2026, and pipeline gas starting June 2026. Regarding long-term contracts, the ban on LNG will take effect at the beginning of 2027, and on pipeline imports starting from October 1, 2027. Landlocked countries will receive a one-month extension, until November 1, 2027, provided that the country needs to fill gas storage facilities ahead of the winter energy peak season.

In addition to EU member states, other Western nations have joined the sanctions. In 2022, the US, Australia, Canada, the UK, and Switzerland introduced bans on import of all Russian energy resources.

In September 2022, the G7 coalition decided to implement a centralized price cap on oil and petroleum products of Russian origin. It entered into force on December 5, 2022, establishing that Russian crude oil could not be purchased for more than $60 per barrel. In 2025, this cap was made more flexible, fluctuating at a level of 15% below the average global Brent price. According to the original design, the floating cap is to be reviewed every six months to align with current market conditions. As of September 2025, and until the next rate review, the cap was reduced from the initial $60 to $47.6.

Service providers from the Price Cap Coalition (comprising the G7, the EU, and Australia) are prohibited from providing transportation, insurance (including P&I reinsurance), and financing services to actors selling Russian oil at a price exceeding the established cap. By doing this, the specified countries aimed to limit Russia's oil export revenues while maintaining the availability of Russian supplies on the global market to avoid a sharp spike in energy prices.

In January and October 2025, the US added key Russian oil companies—Surgutneftegas, Gazprom Neft, Rosneft, Lukoil, and their subsidiaries—to the Specially Designated Nationals (SDN) list. Consequently, US citizens, companies, and financial institutions are prohibited from engaging in any activity with these entities, including dollar transactions, logistical operations, and insurance of assets and cargo. Concurrently, the EU included these companies in its sanctions lists, restricting their access to European ports and financial services, including insurance and brokerage.

In December 2025, the Council of the European Union and the European Parliament reached an agreement regarding the final phase-out of energy imports from the Russian Federation. LNG imports are scheduled to terminate in December 2026, followed by pipeline gas in September 2027.

Russia’s Adaptation to New Conditions and Circumvention Practices

Prior to the introduction of the sanctions framework and the adoption of the strategy for energy independence from Russia, EU member states were the primary importers of Russian oil and gas. According to the US Energy Information Administration estimates, in the early 2020s, half of all Russian crude oil exports were directed to Europe, whereas by 2025, this share had decreased to just 11%. Only standalone supplies via the Druzhba pipeline remain.

In view of sanctions and a declining demand, Russia was forced to promptly seek new markets for oil and gas. This led to a reorientation of exports toward Asian countries, primarily China and India.

Simultaneously, Russia developed mechanisms to circumvent dollar transactions, which increased the significance of other currencies in Russian oil trade (the yuan, rupee, and dirham). According to the Russian Ministry of Energy, the share of the dollar in oil transactions fell from 55% to 5% between 2022 and 2025; meanwhile, the share of ruble transactions reached 24%, and yuan transactions reached 67%.

Additionally, following the imposition of US sanctions, Russia significantly increased cooperation with small independent refineries in Asian countries, as they remain willing to purchase Russian feedstock despite the risks of secondary sanctions.